PDFelement - Edit, Annotate, Fill and Sign PDF Documents

Get from App Store

If you are the executor of an estate, using IRS Form 706 will help you in establishing the value of that estate. When a person passes away, their inheritors get what is known as a "stepped-up basis." For example, the cost basis is attuned to the present fair-market worth of the congenital property. The date at which that stepped-up estimation is calculated is either the date of death of the descendant or exactly 6 months after they died.

If at some point you will need to fill out an IRS Form 706, filling out with Wondershare PDFelement would be your best bed. This software is all-in-one PDF filler that supports both Mac and Windows PC. Aside from letting you fill out your form, it also allow you to modify size, text, color, delete text, add text, insert, crop, insert watermarks, resize crop pages, delete images, extract, and a lot other features.

Key Features

Step 1: Download the IRS Form 706 from the IRS website and import the downloaded file on Wondershare Element.

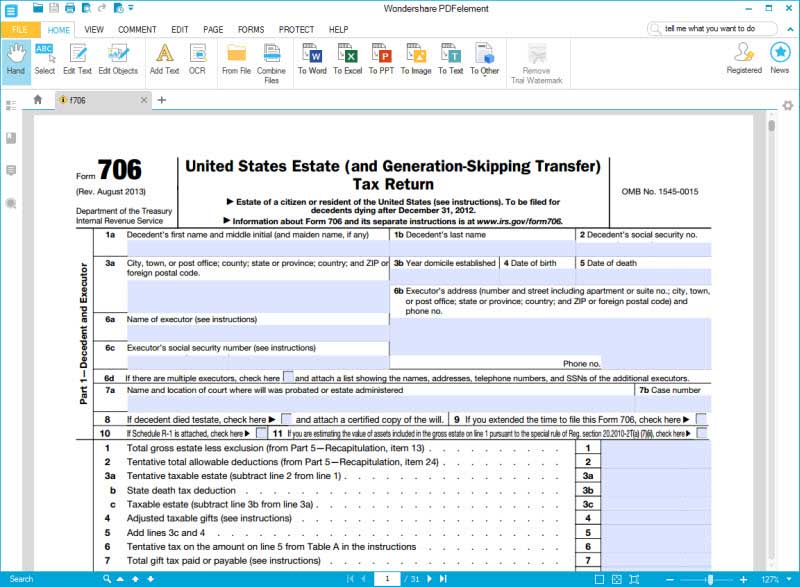

Step 2: Write Information about Decedent and Executor.On the first part of the Form 706, you have to write the name of the descendant, as well as his or her home address, Social Security number, year domicile was established in the his or her state of residence, date of birth, and date of death. On the line 6a, you can write the executor you would like to be contacted by the IRS; list any additional executors on an extra sheet as an exhibit and imply it here. The other of the Part 1 is pretty self-explanatory.

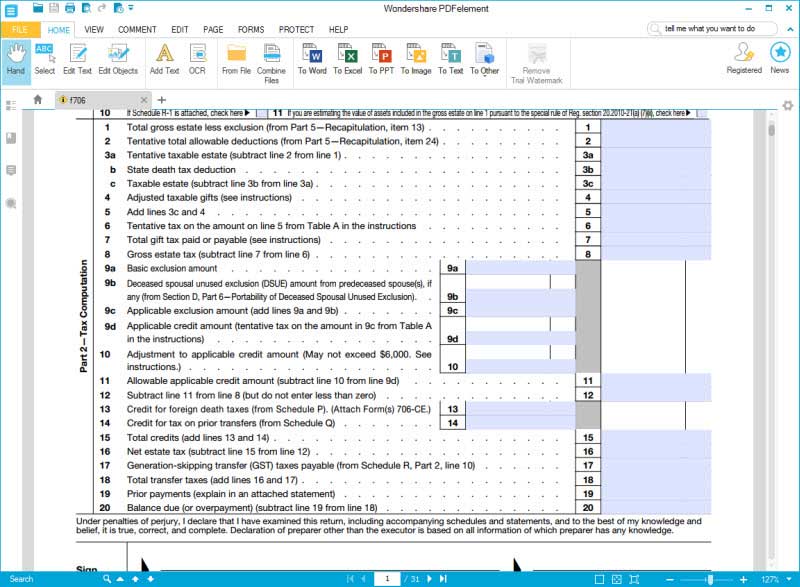

Step 3: Tax Computation.In this part you have to start dealing with the numbers. But you have to know that even though this section is on the first page of the form, you cannot do anything with it until you have finished everything else.

You need the form 709 of the descendant in order to complete the worksheet. Remember that besides any gifts reported on the form 709, you have to include any taxable gifts from prior years that you are aware of that were not reported on the form 709 but should have been.

If ever you stumble upon gifts from earlier years in the papers of the descendant that were not reported, keep count year by year in order to see if they are taxable. The yearly exclusion amount has changed throughout the years, so you have to look on the instructions for that specific year’s709.

Step 4: Use the Line 7 Worksheet.If the decedent had a spouse that died on or after January 1, 2011, you must weite the deceased spousal unused exclusion on the Line 9b, if any, from Section D, Part 6-Portability of Deceased Spousal Unused Exclusion. On the Line 10, you must write adjustments to the applicable credit amount. You have adjustments just if the decedent sent gifts after September 8, 1976, and before January 1, 1977, for which he or she requested a precise exemption. If so, the combined credit on the estate tax return is reduced. Calculate the reduction by writing 20% of the precise exemption that was demanded for these gifts.

On the Line 13, you must enter any credit for foreign death taxes from Schedule P and ascribe Form(s) 706-CE. On the Line 15, you must add lines 13 and 14 in order to get the total credits. On top of using line 15 to report the totals of line 13, credit for foreign death taxes, and line 14, credit for tax on previous transfers, you might also use it to take a credit for pre-1977 federal gift taxes below a formula laid out on page 9 of the Instructions

Step 5: Get the signature of executors. You have to get all executors or administrators sign and write date the return at the lower part of page 1, even though only one signature is necessary. If nothing exists, the person or persons holding assets who is or are submitting the return like the trustee or trustees of a trust, sign.

Step 6:Make the preparer sign other than the executor.If you paid another person to prepare the Form 706 for you, then that person has to sign the return and completes it in line with the Instructions.

Still get confused or have more suggestions? Leave your thoughts to Community Center and we will reply within 24 hours.