PDFelement - Edit, Annotate, Fill and Sign PDF Documents

Get from App Store

To report the earnings (that is accumulated, distributed among worker and the amount that is help for future uses), gain and loss, trust, deduction and bankruptcy of an estate you need to use Tax Form 1041. Both Estate income and trust can be calculated by following the same procedure as we do for the individual incomes and with all the credits and deduction allowed are same. The only big difference is that a decedent's estate or a trust can take a distribution of income that is deducted to beneficiaries.

IRS Form 1041 is a very important document that should be handled with care. You one software that has made filling this complicated document into an easy one is Wondershare PDFelement . This is one of the easy to use PDF editor and creator. It has many up-to-date features that will allow you fill the legal documents easily.

Key Features

Once you have the form, you can open them in the Wondershare PDFelement.

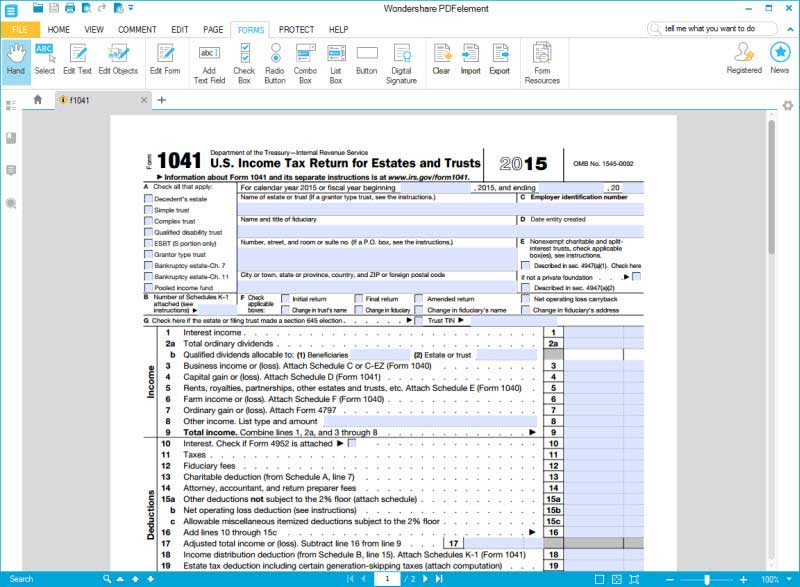

How to fill Column A?

Check all the boxes that are applicable in Column A.

Where to Enter Your Personal Details

To the left, you need to enter the details including the name and address of the estate.

How to fill Column B?

Enter the details of K-1 Schedules

How to fill Column C?

Further left, you can see the column for employment identification number.

How to fill Column D?

Below that is Date on which the entity was created.

How to fill Column E and F?

Check the boxes that are applicable for in the columns E and F. Column E is for split-interest nonexempt trusts.

How to fill Column G?

Check it if you had made a 645 election in your organization.

How to fill columns with Income details?

Below that is the column to enter the income details. You need to enter the details like Interest income, Qualified dividends allocable, Total ordinary dividends, royalties, Rents, partnerships, Business income or (loss), other trusts and estates, Total income and others.

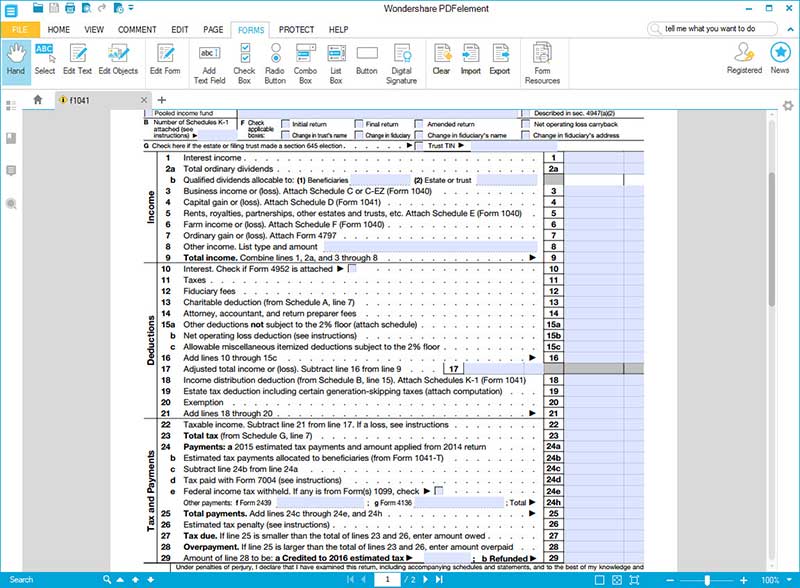

How to enter the Deduction Details?

Below that is the column to enter the details about deductions. Answer the questions from the lines 10 to 21, which include, Taxes, Attorney, Charitable deduction, accountant, return preparer fees and Fiduciary fees and the details of Income distribution deduction and other deduction, etc.

Where to enter Tax and Payments details?

Lines 22 to 29 have a series of questions about tax and payments. This includes Total tax amount, Estimated tax payments allocated to beneficiaries, Federal income tax withheld, Total payments, Estimated tax penalty, Tax due and a few other details as well.

Schedule A: Charitable Deduction

Then we move to the page 2, which starts with the section Charitable Deduction. If you are filling for a pooled income fund and simple trusts, this can be avoided. This has following questions in it the capital gain that is paid after excluding allocations for section 1202 or the amount that is allotted for permanently for the charitable purposes. There are also questions regarding the income that is exempted by tax and will come under charity, The amount of capital gain in an that is kept aside for corpus and are paid or allocated for the charitable activates, the amount that is reduced for charitable activity. Amount that has been paid for charity from the total gross income can be calculated by taking the difference of the amount form 6th line and 5th line. This is the amount that you will enter in the 13th line of page 1.

Schedule B: Income Distribution Deduction

Schedule B is to be filled with the details of Distribution Deduction of the income. You will have to answer the question of Adjusted total income, how much is the net gain that you can find from the Form 1041’s schedule D, Adjusted tax-exempt interest, line 19, column (1) and other details as well. This includes the amount of Capital gains for the tax year included on Schedule A, line 1. If you get the value of line 4 in page 1 as gain, then you need to show this as a negative one. If you have received a loss, then you need to show it as a positive one.

Net income that is distributable, which is a combination of lines 1 to 6. In case, it is 0 or a negative, enter -0-. In the next line, you have to answer only if you are a complex trust, and then, you need to enter the value that come as the accounting income. A governing instrument determines this. It comes under a local law. Other amounts paid, distributed, credited amounts and income that is needed to be distributed are also entered here.

Schedule G Tax Computation

Schedule G deals with the Tax Computation, where you have to answer questions about Tax, tax credit by a foreign agency, Net investment income tax that can be found in the Form 8960, Recapture taxes and other.

Other information

This is followed by series questions in the section other information, where you have to answer a few more questions that include the amount of tax-exempt income the trust or estate receives, whether the trust or estate receive any part of the income. There are about 9 questions.

Still get confused or have more suggestions? Leave your thoughts to Community Center and we will reply within 24 hours.